Illinois Homeowner Protection Notice

Everyone is aware of the current housing crisis. Families everywhere are struggling to meet their mortgage payments. Banks are overwhelmed by the number of requests for loan modifications and understaffed for the task. Working out a solution to save your home often means looking for more time: more time to negotiate a modification, more time to try to short sale your home, more time to try to save up money for a housing transition.

Everyone is aware of the current housing crisis. Families everywhere are struggling to meet their mortgage payments. Banks are overwhelmed by the number of requests for loan modifications and understaffed for the task. Working out a solution to save your home often means looking for more time: more time to negotiate a modification, more time to try to short sale your home, more time to try to save up money for a housing transition.

To prevent hasty foreclosures without homeowners getting information they need to assess how to move forward, the Illinois legislature instituted a homeowner protection notice. Located at 735 ILCS §5/15-1502.5, the homeowner protection notice became law in April of 2009 and is set to expire July 1, 2013.

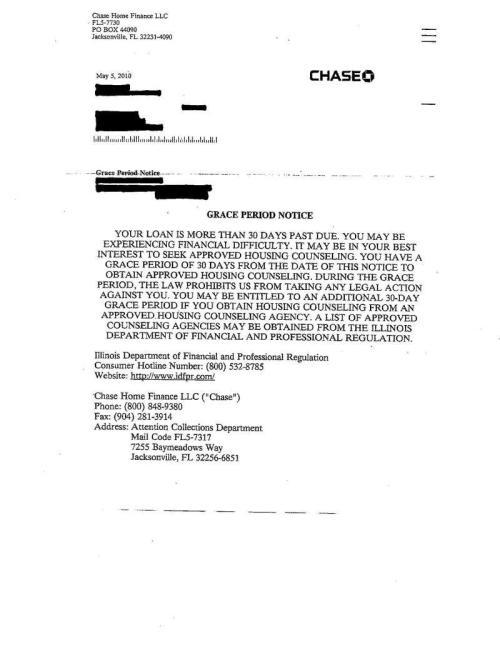

The new law requires banks foreclosing on mortgages to send a notice to the homeowner that looks like this:

The notice is required to contain certain information. Including, for example, the fact that the loan is past due, that approved housing counseling is available, that attending the approved counseling will create an additional 30 days of grace, and contact information to set up a counseling session.

One of the biggest advantages of this notice provision is that it creates additional time for homeowners to research the options available to them before a foreclosure action is initiated in court. It also creates a valid defense in court for homeowners who never received the required notice. If you find yourself in court facing foreclosure and you never received this homeowner protection notice, you can challenge the validity of the foreclosure process. The bank is strictly prohibited from filing a court action for foreclosure until this notice is sent and the homeowner has the opportunity to schedule a counseling appointment.

Concluding remarks: The Illinois legislature wants to see homeowners protected from losing their homes. If your home is in distress and you are behind in your payments, be on the watch for this notice from your bank. Then set up a counseling session. Not only will you become more educated, you will have a little bit more time to plan your next step.

Foreclosure

Foreclosure